Bond Pricing System

Redesigning how investment bankers price bonds

background

A pricing sheet is a real-time debt scenario used to evaluate potential new debt issuances. Prepared by junior bankers, these documents are sent to clients weekly as market updates or included as part of a larger deal deck. Their accuracy is critical as they directly inform client decisions on timing and structure of new bond issuances.

problem

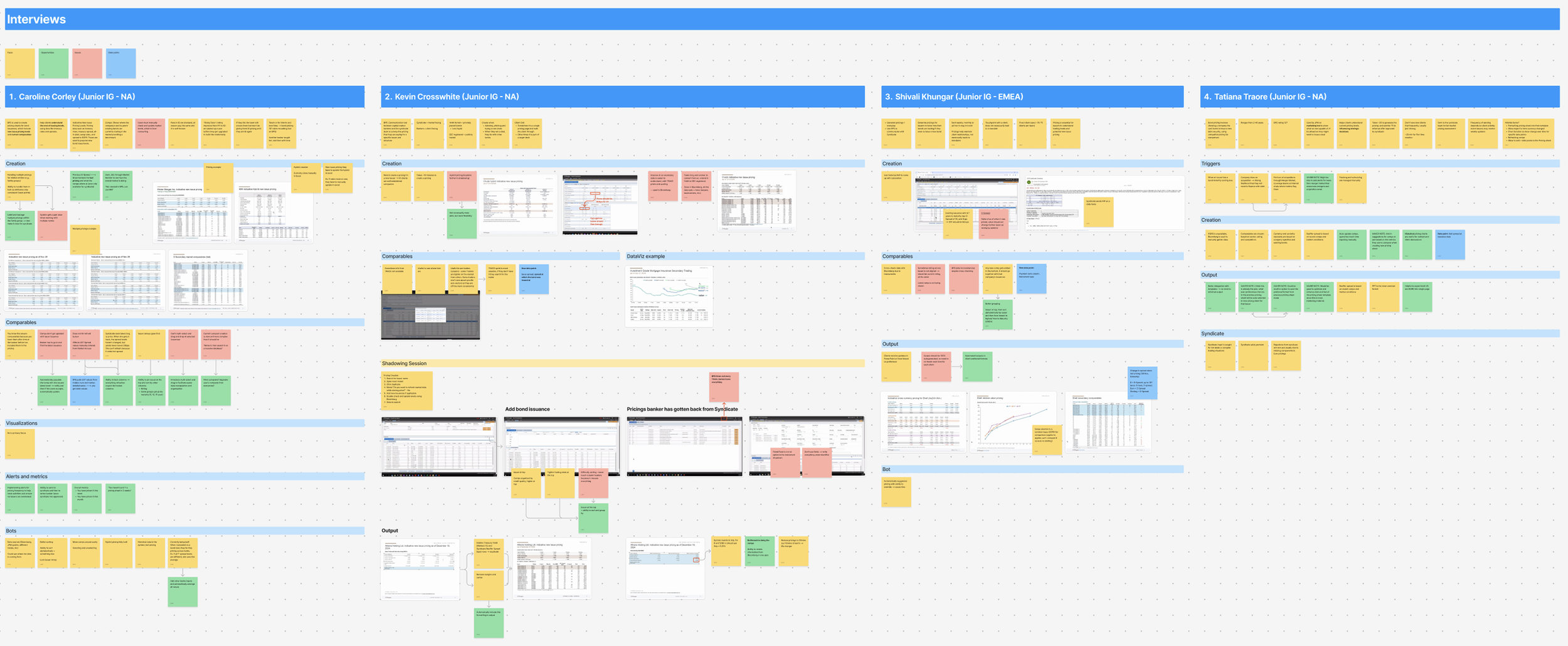

Generating a pricing sheet required junior bankers to manually check and re-enter data across four separate systems, a process that took ~30 minutes per sheet. Beyond the time cost, manual data entry introduced the risk of human error in a context where accuracy is non-negotiable. There was no single source of truth, no way to catch anomalies at a glance, and no standardization across the team.

How might we automate the bond pricing process to reduce manual data entry and improve accuracy?

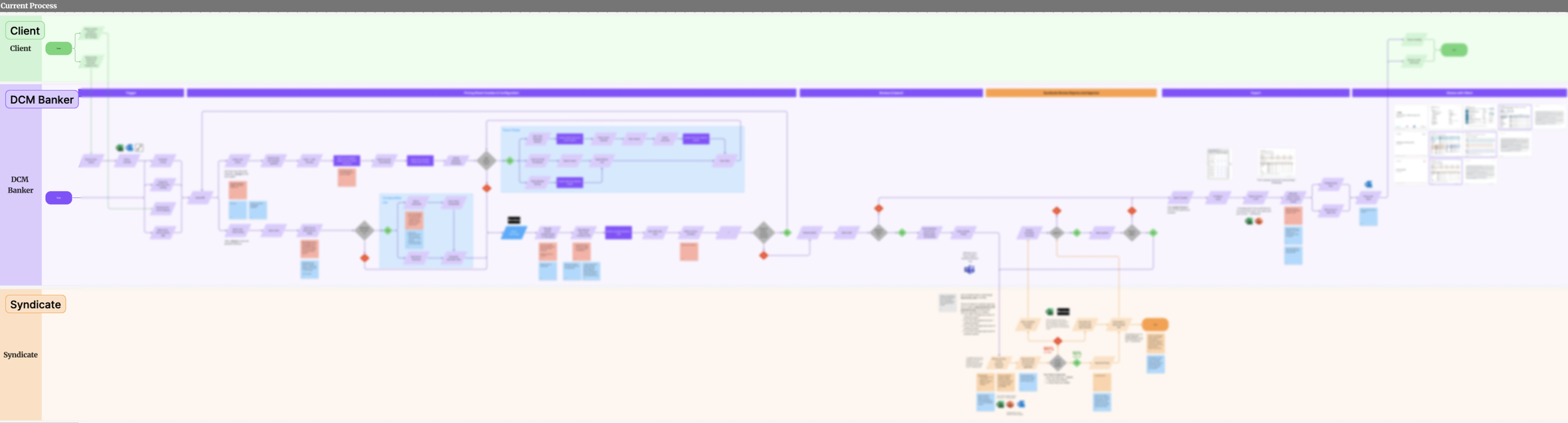

Current process

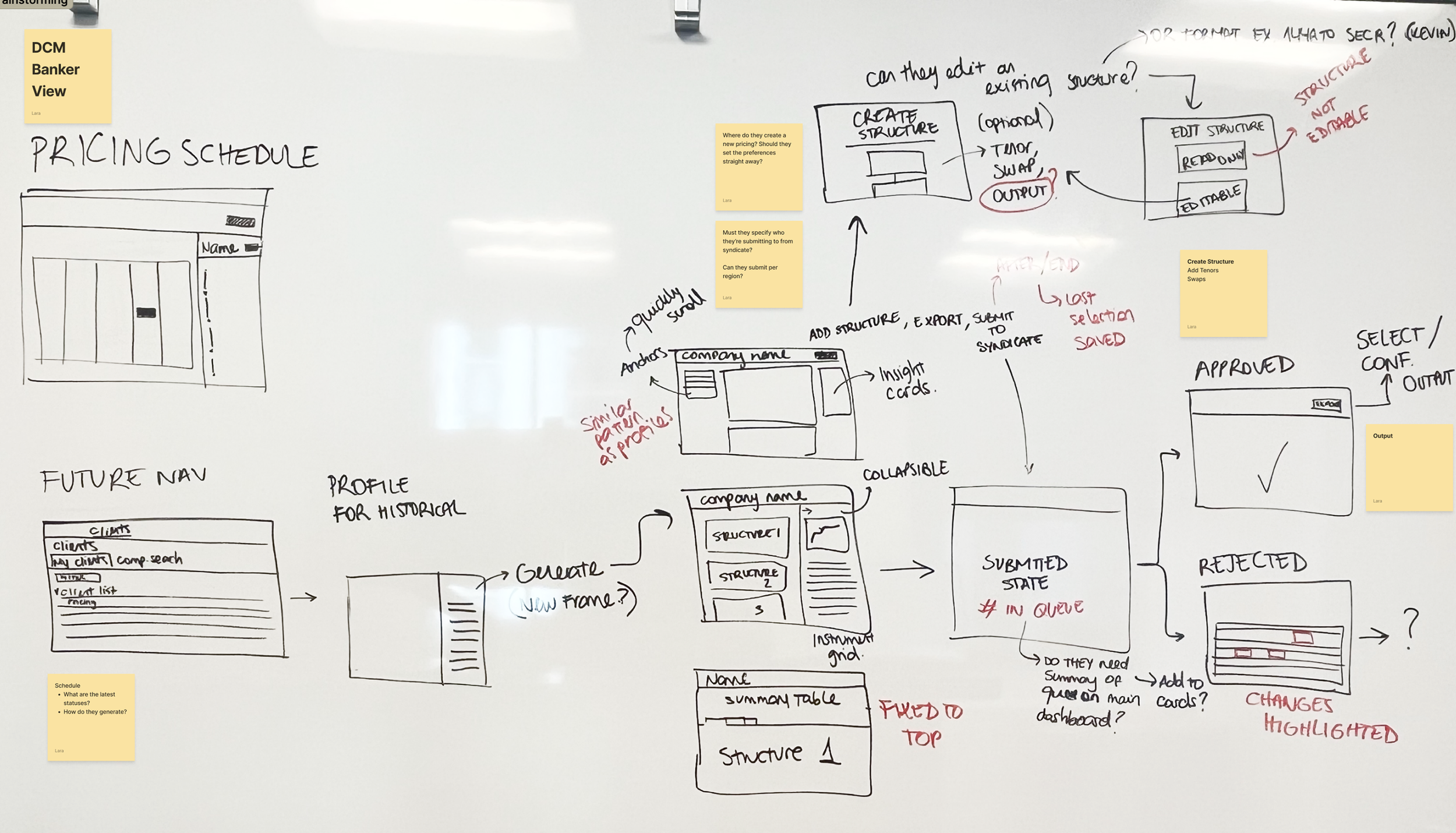

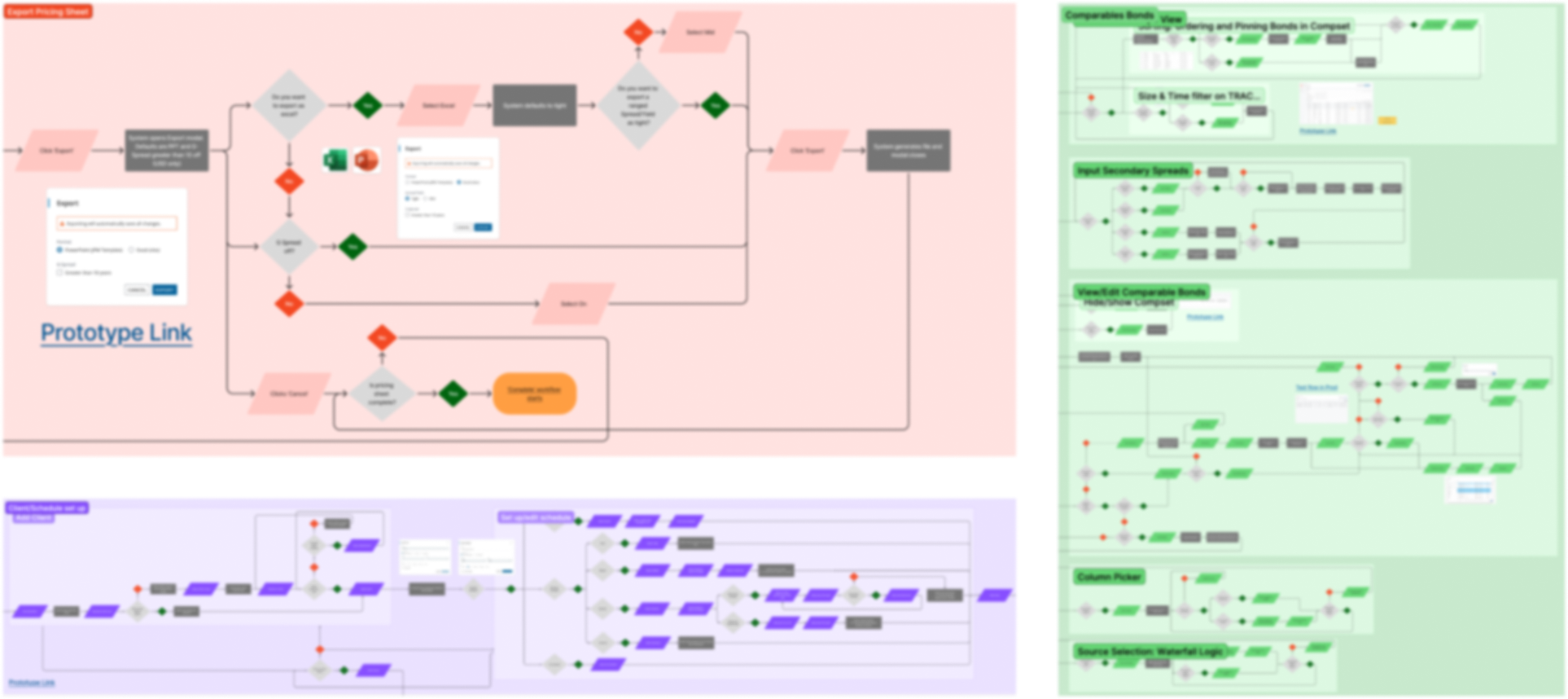

End-to-end lo-fi prototype

End-to-end low fidelity prototype tested with DCM and Syndicate bankers.

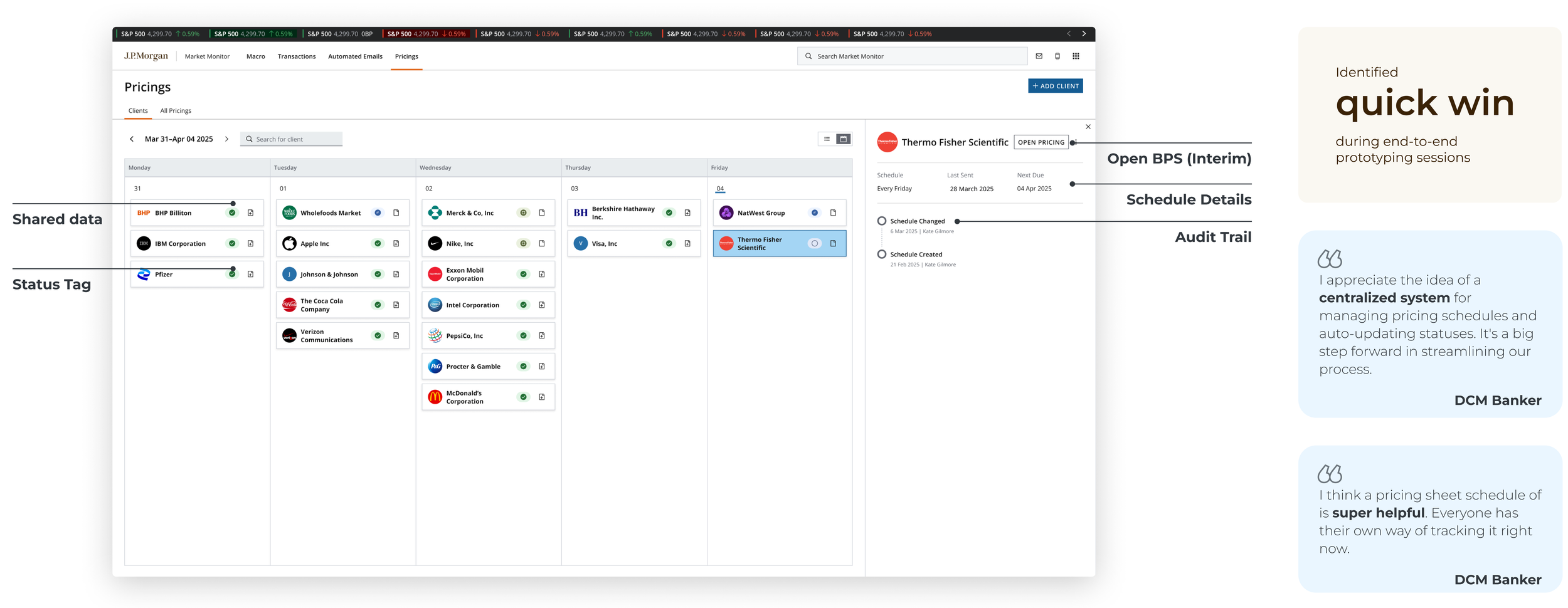

Quick Win

During low-fidelity feedback sessions, bankers revealed they were each tracking pricing sheets in their own way. No standardization, no shared visibility. This surfaced a quick win: a centralized pricing schedule that could be scoped and shipped immediately, while the core data infrastructure was being restructured.

New WORKFLOW

End-to-end workflow mapping including all user and system actions. Blurred for confidentiality.

Final deliverables

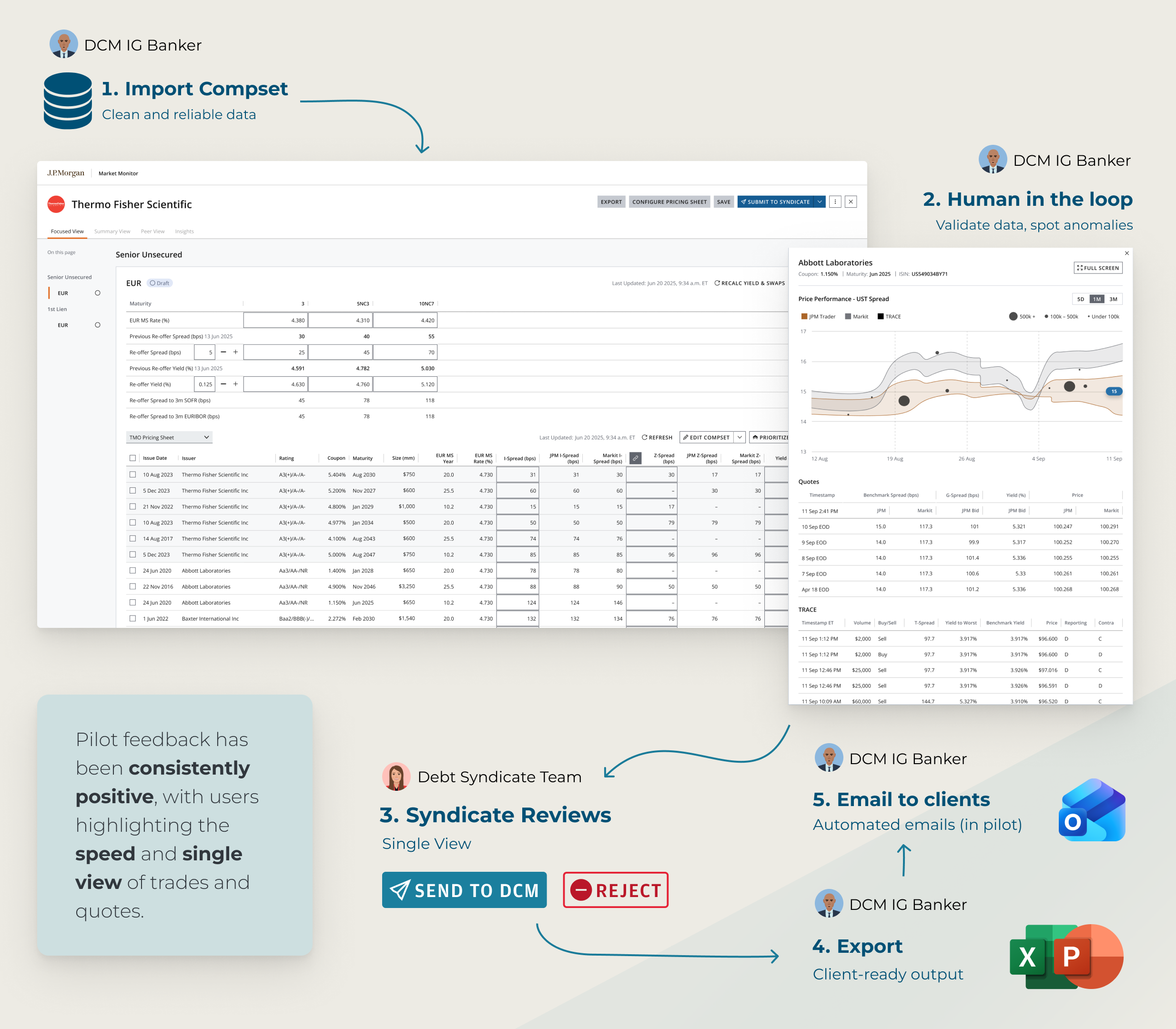

The Bond Pricing System consolidated the fragmented workflow into a single platform. The solution comprised three core components:

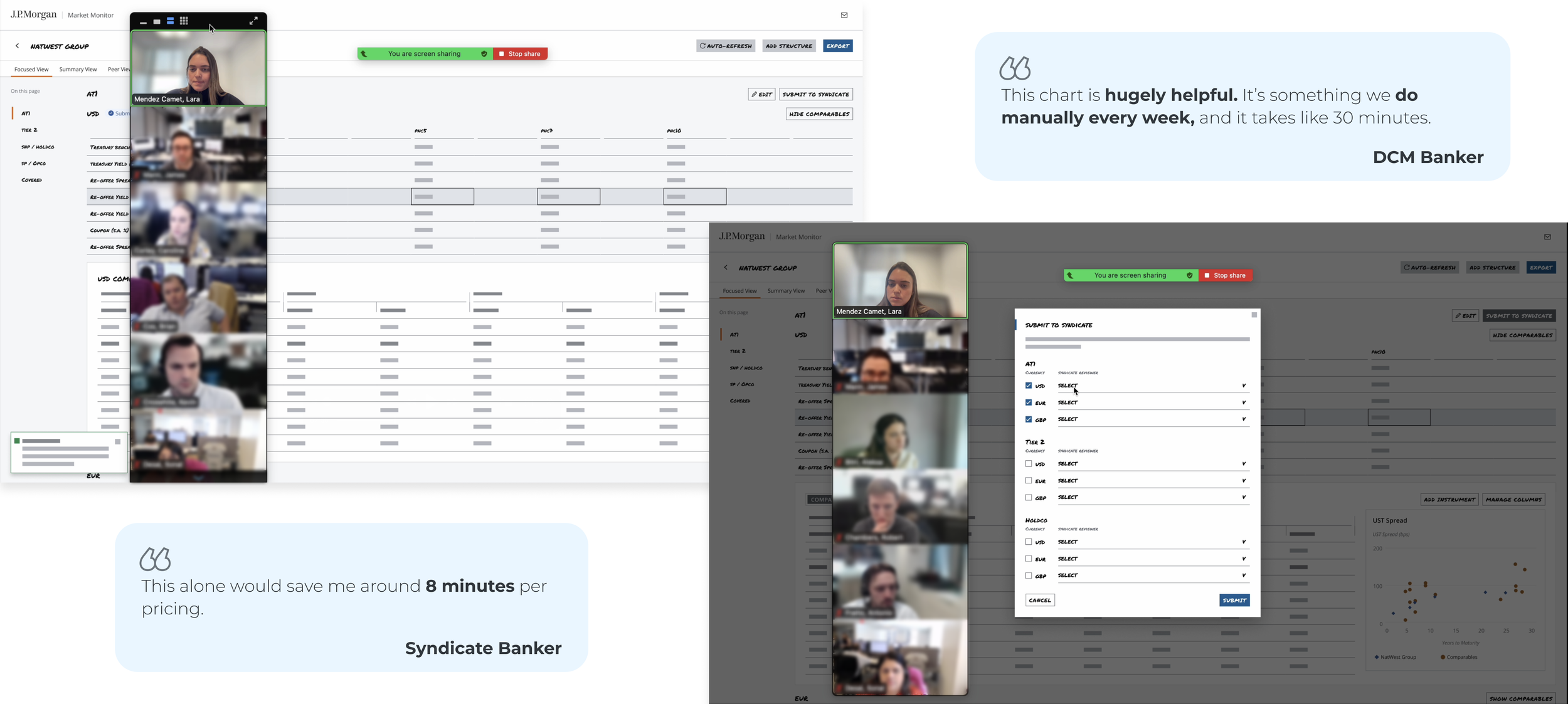

Automated comparables set creation

Data is pulled and populated automatically from verified sources, eliminating manual re-entry across systems.

Data visualization layer

Visual representations of pricing scenarios allow bankers to identify anomalies at a glance, rather than reading through raw numbers line by line.

Unified workflow

A single surface replacing the previous four-system process, reducing cognitive load and standardizing output across the team.

Outcome

The pilot launched for USD pricing in February 2026. Time to complete dropped was reduced by 70%. Data accuracy improved through auto-population from verified sources, reducing the risk of manual entry errors.

Pilot feedback has been consistently positive, with users highlighting the speed and single view of trades and quotes. We are continuing to gather feedback before expanding to additional insights, automation, and other currencies.